![]() How much should I save for retirement? How much should I increase my contributions when I get a raise? Should I save in my firm’s 401(k) or a personal IRA? Which investments should I choose?

How much should I save for retirement? How much should I increase my contributions when I get a raise? Should I save in my firm’s 401(k) or a personal IRA? Which investments should I choose?

For many of us, making the right choices when navigating the bewildering world of investing for retirement can seem nearly impossible. We know that correctly answering these and other questions that arise when investing for retirement are the keys to a comfortable living during our golden years, yet it often feels as if we’d need a finance degree to do so.

Unfortunately, there’s one crucial question which most of us didn’t even know we should be asking, but may have been the most important one of all: are the retirement investment options in my 401(k) or those recommended to me by my financial advisors the best available? Regrettably, until now, the answer very well may have been “no.” However, thanks to a new rule called the fiduciary rule announced by the Department of Labor today, it may soon be “yes.”

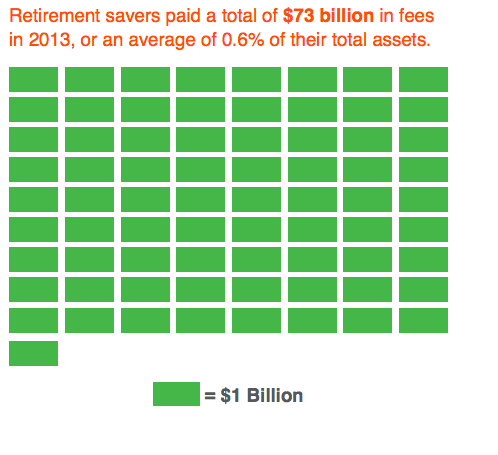

What is the fiduciary rule, and how will make saving for retirement easier? For a more in-depth description, you can check out this fiduciary rule explainer that we wrote last year. But in short, every retirement investment option, from index funds to money market funds, charges savers a variety of fees for everything from investment management to advertising. These fees, which can reach as high as 2 percent per year, may not seem all that significant–but over time, they can really add up. In a previous report, we estimate that they can cost an average, diligently saving household over $150,000 by the time they retire. All told, retirement savers paid a total of $73 billion in fees in 2013.

Here’s where the fiduciary rule comes in. Some of these fees are necessary—accounting costs, some investment management expenses, etc—but a big portion of them are incurred because financial professionals aren’t required to recommend the investments that are the best deal for savers; instead, they often recommend the funds that earn them the largest commissions, which in turn get passed on as fees to folks struggling to save for retirement. How much is such bad investment advice costing savers? The White House estimates about $17 billion a year; our own estimates indicate it could be as much as $25 billion.

The Department of Labor’s fiduciary rule, the final version of which was announced today, will eliminate these excessive fees by requiring that financial advisers recommend the best retirement investment options for savers, not the ones that line their own pockets. And while there are many other problems with our country’s individualized retirement system—detailed in our report on 401(k)s’ many flaws—the fiduciary rule is a huge step towards a retirement system that works for all Americans.