The Affordable Care Act, or Obamacare, is now underway. If you are among the majority of Americans who already have health insurance, not much will change. But there will be one big plus: no insurer can refuse you or raise your rates because you are or have been sick. Your cost will probably go down, too. If you are among the 48 million Americans who don’t have insurance, the program is meant to help you get it.

Click through for a larger image

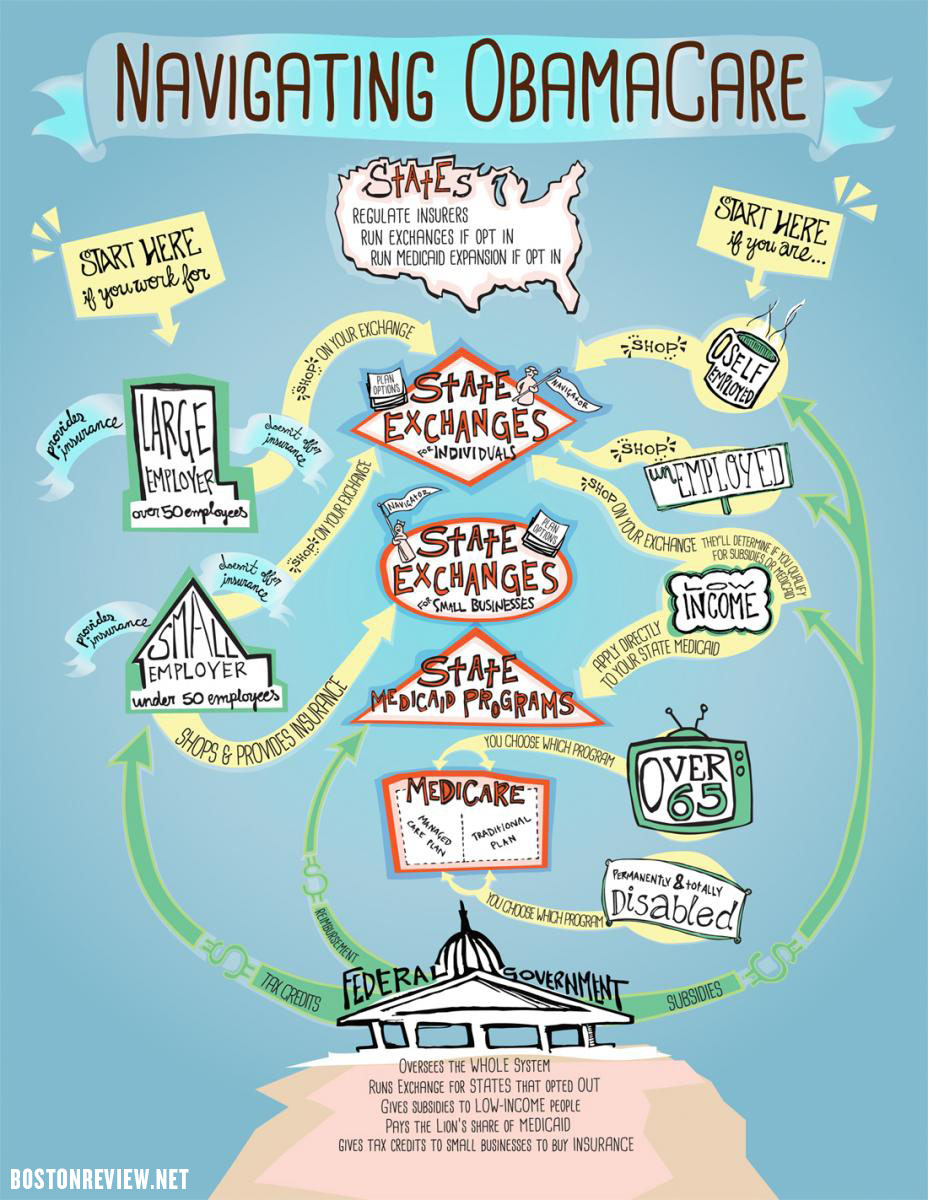

Who are you in the eyes of the ACA?

- If you work for an employer who already provides health insurance, you are all set. If not, you can shop on the individual exchange.

- If you work for a small company that does not provide insurance, take heart. In each state, a small business exchange with the zippy acronym SHOP vets commercial plans that small business owners can purchase for their employees. If your employer chooses not to take advantage of SHOP, you can go to the individual exchange.

- If you are over 65 or permanently and totally disabled, you will be insured through Medicare.

- If you are self-employed, unemployed, or have little income, you likely will be able to get insurance through your state exchange or Medicaid program, though it will be harder in some states than others.

Your State Health Exchange

Exchanges square the political circle of creating a public insurance program through private business. An exchange is an online marketplace where government officials vet private insurance plans to make sure they provide essential coverage at affordable prices.

Hitch #1: 34 states chose not to set up an exchange and let the federal government run it for them. The federal exchange went online on October 1 and has since been swamped with people seeking insurance, trying to find their way among the 17,000 plans posted on its Web site. Whether your exchange is federally or state run, you can get human help from “navigators.”

Hitch #2: some Republican-controlled state governments are doing everything in their power to keep the exchanges from working. Florida prohibited the insurance commissioner from approving new premium rates, so Floridians won’t see any lower prices from competition. Several states prohibit navigators from operating in public hospitals or giving advice, and a few have set onerous licensure requirements for them.

Hitch #3: in some states, few insurers have signed up, meaning there is little choice for residents. In New Hampshire, for example, there is only one insurer, and it won’t cover care in 12 of the state’s 26 hospitals.

Despite all the hitches, people are going to the exchanges in droves. Millions of people visited the federal Web site on the first day, overwhelming the site. State-run exchanges are going more smoothly. In New York state, 40,000 people applied for insurance in the first week. In Washington state, 9,400 people.

How to Get Medicaid

Under the ACA, Medicaid was supposed to cover about 16 million more uninsured people. This would be accomplished by raising the income eligibility level to 138 percent of the federal poverty line, about $16,000 for one person. But 26 states—the ones with the most uninsured people—are refusing to expand their programs. Poor, uninsured blacks and single-mothers will be disproportionately left out because two-thirds of them live in these 26 states.

But there is a ray of hope: because the federal government covers 90–100 percent of the cost of new enrollees, most states will probably sign on eventually, especially now that the administration says states can use federal money to buy private insurance for their Medicaid enrollees.

Follow the money

The ACA is billed as creating an expanded marketplace, but don’t think of it as a Wal-Mart handling simple cash deals. The point of this marketplace is to help people who need medical care get it, especially those who can’t afford insurance. The federal government gives subsidies and tax credits to most new insurance buyers. The IRS collects taxes from everyone and nominal penalties from people who don’t buy insurance. Other revenues come from reducing reimbursements to doctors and hospitals. Like every market, this one is a creature of government. That’s the only way to get most currently uncovered Americans health insurance.