California is spending billions to shore up its defenses against heat, flash floods, rising seas and other effects of climate change. But to do this, it is, ironically, working with the very institutions that are financing the fossil fuel activity causing the crisis.

To sell bonds that finance various initiatives, including massive projects that help the state deal with effects of the climate crisis, California relies on banks to find investors willing to purchase them. Bonds are like loans that the state pays back to investors over time, plus interest. Banks that help sell the bonds are “underwriters” for the bonds.

Now the California Legislature is considering a climate resiliency bond worth $15.5 billion. It’d be a general obligation bond, meaning the state can repay it in a wide variety of ways. (Other kinds of bonds are tailored more specifically to certain agencies and institutions, such as public works, veterans affairs and state university systems.) The bond comes in response to Gov. Newsom’s broad budget cuts across the board, including climate resiliency spending, in response to a deficit.

Other bonds, totaling $28.68 billion, are also under consideration by the Legislature for new spending on affordable housing, updating educational facilities, and constructing treatment shelters for people experiencing homelessness. A group advocating for cleaner energy will ask lawmakers to require that any infrastructure built with bond financing be free of fossil fuel gas hookups. Instead, they want new buildings to be electrified and powered with renewables like wind and solar, in line with the state’s decarbonization plan.

By themselves, the bonds are already large compared to previous state bond issuances. If all four pass the Legislature and get approved by voters next year, they would represent the biggest set of general obligation bonds ever issued by the state. Yet to sell the bonds to investors, California may end up paying millions to banks that are also financing oil, gas and coal projects.

Join our email list to get the stories that mainstream news is overlooking.

Sign up for Capital & Main’s newsletter.

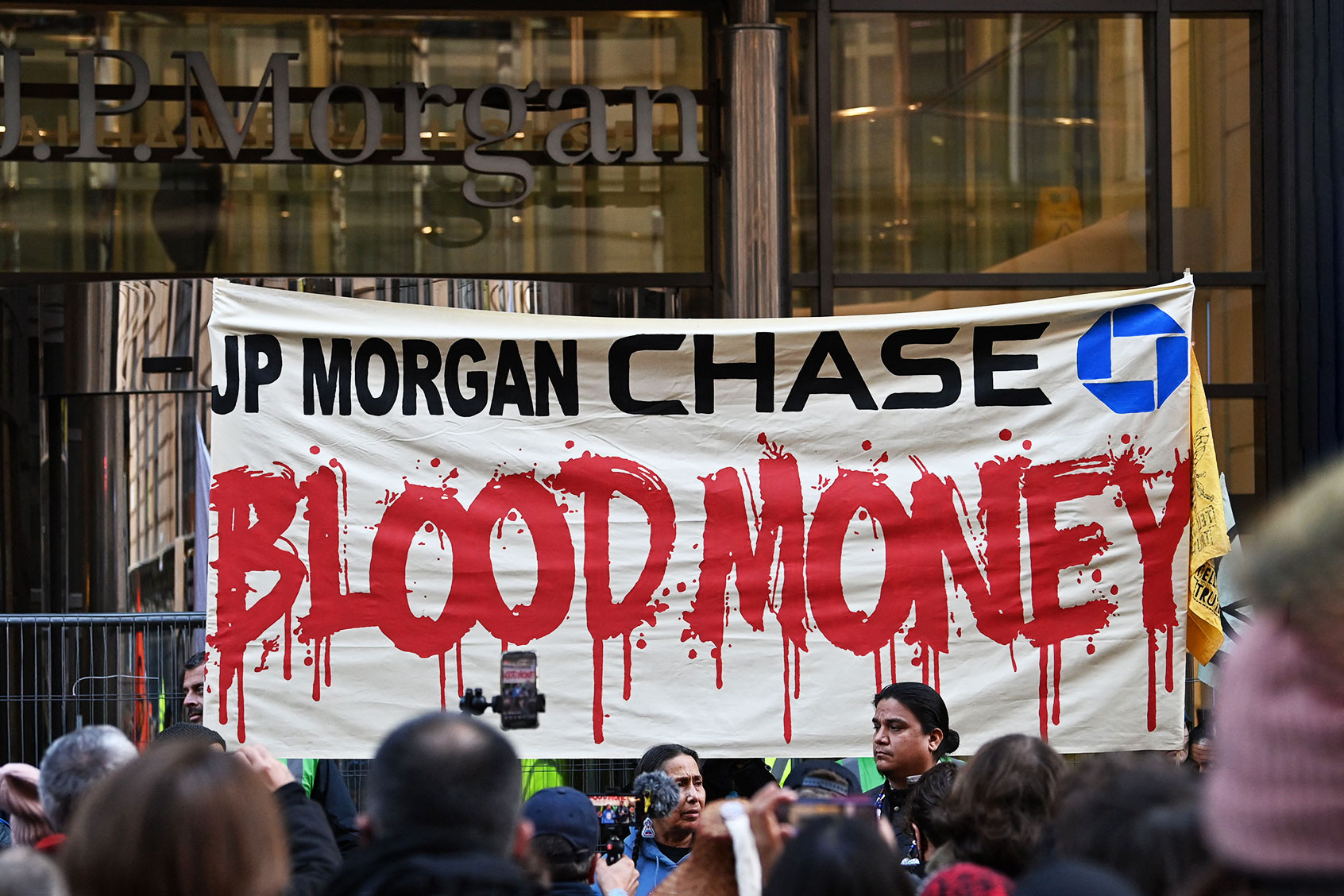

The state is already committed to selling billions of dollars’ worth of climate adaptation bonds thanks to a 2018 measure. The California Treasurer’s Office recently held a sale for bonds intended to mitigate coastal impacts of rising seas, wildfires, drought and flooding. Underwriters included JPMorgan Chase (whose security division is simply called J.P. Morgan), Wells Fargo, Morgan Stanley, Citigroup, TD Group, Goldman Sachs and Barclays.

They are among the banks that sent $742 billion to the fossil fuel industry in 2021, as Capital & Main reported in March. California has paid these banks a total of $73.2 million for underwriting services since 2019.

Some have even worked with fossil fuel producers and distributors in the state. JPMorgan Chase, the world’s leading fossil fuel funder, backed Pacific Gas & Electric with $10 billion; the utility lobbies for fossil fuel gas. Goldman Sachs recently advised Chevron to invest in biofuels refining, which presents its own planet-warming risks, while Morgan Stanley actively recommends Chevron’s stock to investors.

A growing number of banks, all in Europe, have committed to quitting fossil fuels in some form.

For climate activists who want California to sever these ties, it presents a moral dilemma for the banks, which they see as profiting off both sides of the climate crisis.

“California’s investments in climate resilience should not contribute to the profits of banks that are financing the expansion of fossil fuels and undermining California’s efforts to reduce emissions,” said Deborah Moore of the activist group Third Act, which recently held protests against banks invested in fossil fuels.

In addition, members of the Sunrise Project, a group that examines the financial industry’s role in fueling the climate crisis, have argued that California’s economic power enables it to pressure banks on oil and gas if it imposed stricter guidelines for bond underwriters. (Disclosure: The Sunrise Project is a financial supporter of Capital & Main.)

The State Treasurer’s Office chooses underwriters every two years. Among the criteria it considers are competence in marketing bonds, whether a bank is also a creditor of the state and even if a bank has diverse owners. But fossil fuel financing has never been a consideration.

California also contracts with smaller banks that may not hold fossil fuel securities. But Wall Street and large international banks tend to have greater access to potential investors, not to mention political connections and global influence in major ways.

A growing number of banks, all in Europe, have committed to quitting fossil fuels in some form. Nearly half of Europe’s largest banks will now restrict lending for new oil and gas development. France’s La Banque Postale dropped its oil and gas clients in 2021, the first to do so. The commitments are in line with the Paris Agreement of limiting warming to 1.5 degrees Celsius (2.7 F).

Time has likely run out to keep temperatures below this catastrophic threshold; a recent paper authored by dozens of climate scientists suggested we’ll surpass it in 10 to 15 years. Radical societal transformations away from fossil fuels, including many trillions in spending on clean energy technologies and infrastructure, would limit the damage.

Already California has faced up to $100 billion in damages from extreme weather events exacerbated by climate change, such as wildfires and drought, just from 2015-2020.

In response to questions, the California State Treasurer’s Office said that it “understand[s] and support[s] the urgent need to transition from fossil fuels to renewable energy sources to address the global climate emergency and believe[s] the continued greening of our economy, a task our office also assists with in other areas, may have a more meaningful and lasting impact” than excluding fossil fuel financiers from its bond market.

The state treasurer’s greening efforts include sales tax breaks for companies manufacturing battery parts and other renewable energy components and tax-free bond financing for companies implementing certain pollution controls and materials recycling.

The strategy of pressuring banks to take a position on fossil fuels is already in use, but recently more from industry-friendly conservatives. Republicans in 37 states have introduced 165 pieces of legislation proposing to penalize banks, pension funds and other firms for using environmental, social and corporate governance (ESG) criteria to conduct their business.

Texas, for example, banned municipalities from working with banks if the banks restrict lending to fossil fuels or gun companies in some way. The law was written by a think tank funded by fossil fuel companies. It appears to have hurt the state’s economy: The drop in competition for bond underwriters cost Texans $300 million-$500 million.

Whether or not California faced similar consequences from a pro-climate rule for underwriters, divestment supporters say the benefits of fighting the climate crisis outweigh potential losses. Already California has faced up to $100 billion in damages from extreme weather events exacerbated by climate change, such as wildfires and drought, just from 2015-2020. These costs are set to increase.

Other effects, such as rising seas from melting ice at the poles, are happening more gradually but are no less worrisome, experts and land planners say.

During a February presentation hosted by the Coastal Conservancy, which has received $71.5 million from a state climate bond since 2021, U.S. Geological Survey geologist Patrick Barnard described the danger California faces as the Pacific Ocean continues to swallow coastlines.

Sea levels will rise by “a foot over the next 30 years,” Barnard warned. “Bottom line: What we experienced over the last 100 years, we’ll get in the next 30 years, across the country but also for California.”

Read more

about California policy